Bank FDs paid up to 13% and the PPF a flat 12% tax-free in the 1990s — which made fixed deposits the genuinely intelligent choice for our parents. Today the same instruments barely beat inflation. The instrument follows the era. Here is the math.

My father kept almost every rupee he ever saved in fixed deposits, the PPF, and the NSC. He never bought a single share with conviction. And for his time, that was not the cautious choice. It was the intelligent one.

And do not mistake that for ignorance. He knew the stock market existed — he even stepped into it once, leaned on a broker's advice, and lost a lakh or two before quietly shutting that door for good. He was not a man who feared shares because he did not understand money. He understood money deeply. Equity was simply outside his circle of competence at that point in his life, and he was wise enough to know it and stay out. Walking away from a game you have not yet learned to play is not fear. It is judgment.

I want to say that clearly before anything else, because most finance writing today treats the fixed deposit like a blunder your elders stumbled into. It was not a blunder. It was math. The instrument fit the era perfectly.

The problem is not what your father did. The problem is what happens when you copy the instrument instead of copying the thinking. Let's see why the very same FD that built one generation's security will quietly bleed the next one's.

The era that made the FD the smart money

Picture India in the 1990s. My father had six children, a factory job he had earned the hard way, and one rule he repeated until it was carved into me — never spend more than you earn. So where did a sensible man put his savings?

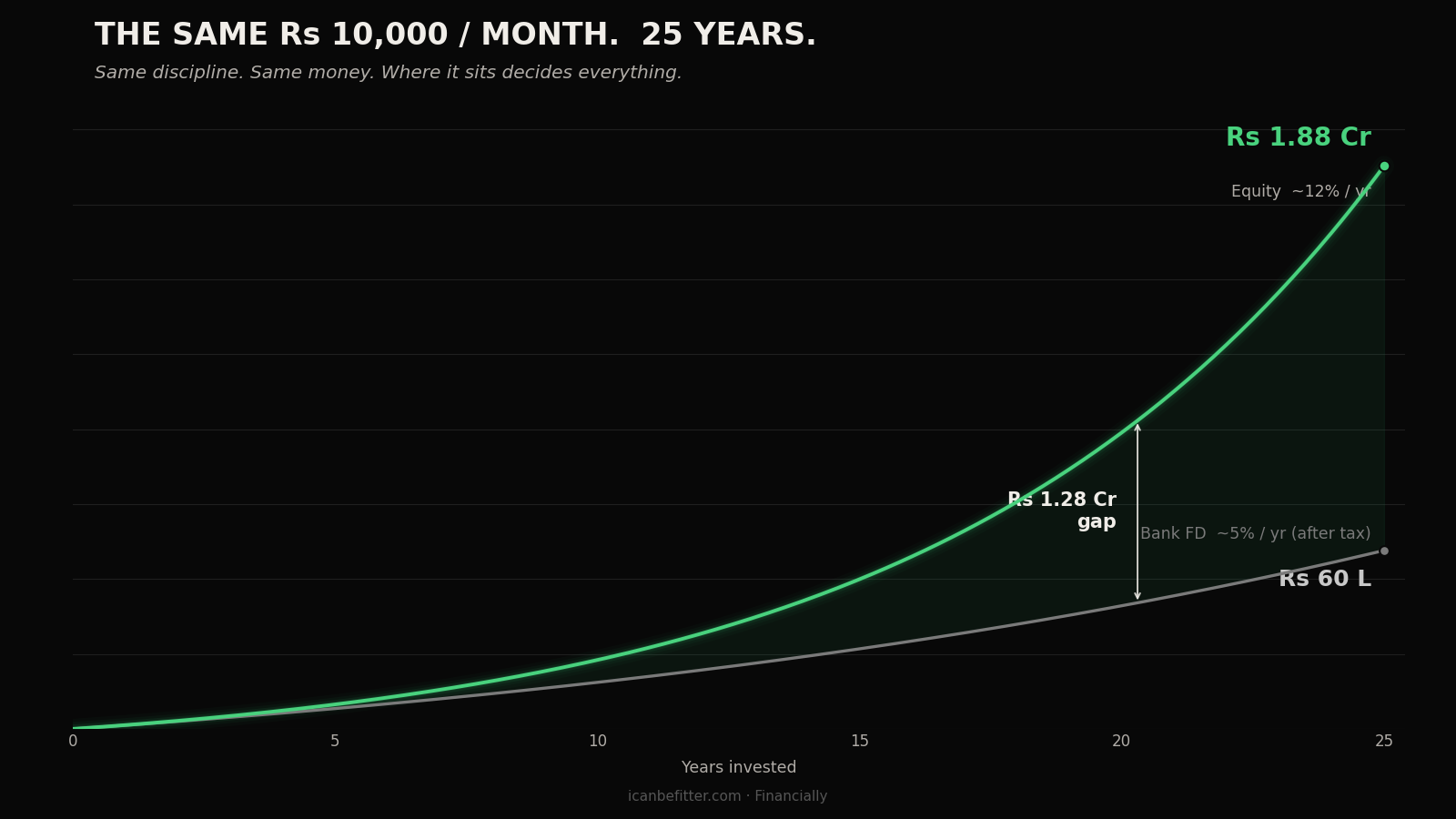

A bank fixed deposit. And here is the number that changes everything: through the 1990s, FDs in India paid ten, twelve, sometimes thirteen percent. The Reserve Bank actually set a ceiling of thirteen percent on deposit rates in 1992 — that was the cap, not the floor. Before the mid-1980s these rates had been held around eight percent; then they climbed and stayed high for nearly a decade.

The Public Provident Fund was even better. From 1 April 1986 all the way to January 2000, the PPF paid a flat twelve percent — and it was completely tax-free.

Sit with that combination for a moment. Twelve percent. Guaranteed. Tax-free. Zero risk. Backed by the Government of India.

That is not a consolation prize for the timid. That is one of the finest risk-free returns any saver, in any country, has ever been handed.

Let's understand what that number actually meant

A return does not mean anything until you compare it to the alternative. So let's do what my father would have done at his kitchen table.

To beat a twelve percent tax-free return using shares, how much would you have needed to earn in the stock market? Tax-free twelve percent is the equivalent of roughly seventeen to eighteen percent before tax for someone in the higher slab. Twelve divided by (one minus your tax rate) — that is the hurdle.

So the question facing my father was simple. Take a guaranteed seventeen-percent-equivalent return with no risk and no effort — or chase the stock market, hoping to clear eighteen percent every single year, carrying all the risk yourself, in a market that was far smaller, far less regulated, and far less understood than it is today.

For a man with six children and no safety net, that is not a close call. The FD was not the safe-but-poor option. It was the high-return option and the safe option at the same time — a combination that almost never exists. He would have been foolish to gamble against it.

He was right. Completely, mathematically right. Behold the rare moment in finance when the boring choice was also the winning one.